I've had my fair share of encounters with Charts of Accounts (COA). I've reviewed them, enhanced them, designed them from scratch, and spent considerable hours reflecting on their nuances. Without a well-structured COA, any attempt to reorganize finance processes or implement automated financial reporting and consolidation is worthless. Whenever I embarked on a new project, I asked for the Group’s Chart of Accounts (Group COA) and the Dimension structure. The insights these documents provide are invaluable! A mere glance can often illustrate the distance a company group has to cross to achieve accurate and efficient automated financial reporting. Dive into this article, and you'll see precisely what I mean.

This article is primarily for multi-entity businesses aiming to transition to automated financial reporting and consolidation. The article provides essential guidelines and best practices for designing perfect Group Chart of Accounts (Group COA), illustrated with practical examples. Perfecting the Group Chart of Accounts is the first crucial step towards automated financial reporting and consolidation.

The article starts by defining the Automated Financial Reporting, then Group Chart of Accounts (Group COA) and its comparison with the Separate Legal Entity COA and the Dimension structure. This leads to the components of the Group COA - the Account Groups and Accounts, and guidelines to consider when designing them. The article concludes with some tips on implementing the Group COA across all group entities. After reading this article, you'll be equipped to define a Group COA for your company, ensuring efficient and reliable automated financial reporting for Statutory, Management, IFRS, GAAP, and Consolidation purposes.

Table of Contents:

Understanding Automated Financial Reporting

At its core, automated financial reporting is the process where financial data seamlessly transfer from a group's individual legal entities (from their respective Accounting, ERP or other systems) into a central reporting platform. This transfer occurs regularly, often daily or weekly, ensuring the data is consistently up-to-date. These data then automatically form reports in a unified format meeting the diverse reporting requirements: be it Statutory, IFRS, GAAP, Group, or Management reporting, including Consolidation. Every number in these reports is backed by detailed transaction-level drill downs.

Advanced reporting systems incorporate automated, built-in and customizable data validation and import checks. These are built-in safeguards that ensure data quality across all legal entities. These systems can detect errors, inconsistencies, missing data, and even silent adjustments to historical data, prompting the respective legal entities to correct these discrepancies before moving forward with data import.

Another significant feature of advanced reporting systems is a customizable foreign currency translation function. This function effortlessly transitions local currency data into the reporting currency right at the point of data import, facilitating real-time reporting, including consolidated views. The reporting systems provide options to customize currency translation strategies for every account in the Group COA, ensuring currency translation in accordance with company needs and consistent application throughout all Group entities. No changing balances for investments, share capital or retained earnings in reports using reporting currency!

Flexible access rights management within these systems ensures that relevant data is accessible to designated users across the entire Group. For instance, a Project Manager can view results for the specific project, a Marketing Manager can review marketing costs for the respective legal entity, and a Group Marketing Officer can access marketing costs for all group companies. Such reporting systems not only promotes transparency but also fosters collaboration and efficiency, as individuals can add comments, explain variances, and adjust forecasts as needed.

The cornerstone benefits of automated financial reporting include heightened efficiency and accuracy. By minimizing manual work of the finance teams, organizations save time and significantly reduce the chances of errors typically associated with manual data entry or computations. Automated reports not only uphold consistency but can also be produced more frequently, even in real-time, offering timely and dependable financial insights.

In essence, automated financial reporting transforms financial data into an always-accessible, dynamic resource, empowering stakeholders at every level with timely and accurate financial insights.

What is a Group Chart of Accounts (Group COA)?

A Group Chart of Accounts (COA), also known as a Unified Chart if Accounts, Multi-entity COA, or Consolidated COA, is a financial organizational tool that provides a standardized template of account codes to be used across different divisions, departments, or subsidiaries within a larger corporation or group of companies, thus streamlining financial reporting. This provides consistency and comparability of financial data across the whole organization and it's particularly useful in multinational corporations where business units span different countries and currencies.

A well-structured Group COA can simplify the process of financial consolidation, help ensure compliance with various accounting standards, and make it easier to generate accurate and timely financial reports for in-depth financial analysis and decision-making.

In the context of automated financial reporting, a Group COA plays a pivotal role. It provides the foundation upon which the imported financial data of separate legal entities are validated and processed by the reporting system. With a consistent structure, the reporting system can accurately compile, analyze, and report financial data across various business units, significantly reducing manual work, potential errors, and time spent on financial reporting tasks.

In essence, a well-designed Group COA is a key enabler of efficient, reliable, and scalable automated financial reporting.

The Distinction: Separate Legal Entity Chart of Accounts vs Group COA

A Chart of Accounts (COA) of a Separate Legal Entity and a Group Chart of Accounts (Group COA) both serve as a financial organizational tool that provides a list of accounts to record transactions in the general ledger. However, they differ in their scope and function.

Separate Legal Entity COA

A Separate Legal Entity COA, or Local COA, is specific to a single legal entity. It is customized to the needs and operations of that particular entity, reflecting its unique structure, financial transactions, and reporting needs. It is usually designed to comply with specific Statutory reporting. In certain countries, statutory requirements rigorously dictate the COA, specifying both account numbers and names. Under such constraints, adapting the account numbers and the account names from the Group COA for individual legal entities becomes unfeasible.

When a Local COA is aligned with or mapped to the Group COA, it often encompasses only a subset of the Group COA, primarily the 'Local' accounts meant for statutory reporting (as demonstrated by LE 1 and LE 2 in the provided example above).

It's relatively uncommon for a Separate legal entity's COA to incorporate accounts for IFRS adjustments or for Cost allocation (see LE3), and if they do, these accounts are typically found in Off–BS accounts not to interfere with statutory reporting.

Group COA

A Group COA, on the other hand, is designed to serve a group of legal entities, such as a parent company and its subsidiaries. In addition to the individual accounts needed by each separate entity for Statutory reporting, the Group COA incorporates accounts that are necessary for group-level reporting requirements, for IFRS or GAAP reporting requirements, for consolidated financial statements (e.g. goodwill, minority interest) and for cost allocation to accurately reflect profitability. There are no globally recognized standards or regulations that dictate the specific content of a Group COA.

Group COA must take into account the diverse nature of the group’s operations, spanning different industries, regions, and regulatory environments, and provide a structure that can accommodate this diversity while maintaining consistency.

Distinguishing Between Group COA and Dimension Structure

Both the Group COA and Dimension Structure are pivotal in the reporting and budgeting processes. They serve as foundational frameworks, structuring financial data in a manner that enhances its clarity and usability for stakeholders.

The Group COA is essentially a systematic list of accounts that form the general ledger of a group. The essence of the COA is to answer the "What?" question. What types of revenue and expense accounts are essential for Statutory, Management, IFRS, GAAP, tax considerations, cost allocations, budgeting, and consolidation?

The Dimension Structure provides greater performance and analytical insights without overburdening the COA. The Dimensions address the questions such as "Who?", "Which?", "How?", and "Where?". For example, Which product generated this sales revenue? Which department incurred this teambuilding expense? Who was responsible for this travel expense?

The Group COA combined with the Dimension structure offers a matrix perspective on the Profit & Loss statement, granting a more comprehensive insight into revenue and expense structure. When both the COA and Dimension structure is well-designed and contain all requisite details stakeholders might seek, setting up automated reports leveraging these two elements becomes a straightforward process.

Example 1

When a dimension structure clearly defines 'Administration' as a Department or Cost Center, there's no necessity for detailed accounts in the COA like 'Administration Salary expense', 'Administration Salary taxation', or 'Administration Bonuses'. In the picture below Administration salaries for Legal entity MD001 are recognised in Department '26ADM - Administration department', consisting of two Cost Centers: 'ADFIN - Finance Teams' and 'ADOTH - Other Administration Teams'.

Deeper analysis of the Dimension structure will be addressed in upcoming article. The next sections of this article will go into more detail on how to design, implement, and maintain an effective Group COA.

Guidelines for Designing the Perfect Group COA

Automated financial reporting transforms financial data into an always-accessible, dynamic resource, empowering stakeholders at every level with timely and accurate financial reporting, giving insights into every financial figure up to the very transaction level. In addition to achieving core business objectives, such as efficient reporting and accurate representation of the Group's financial operations, a crucial aspect of the Group COA is its user-friendliness. Users should easily understand the breakdowns of financial figures by transactions and usage of accounts, account groups and dimensions within automated reports they access.

Examples 2-4

Formulating Account Groups

When preparing the Group COA, it's often best to begin with Account Groups. These groups categorize and summarize all accounts in Group COA in logical order. There are the guidelines to consider for designing effective Account Groups both for P&L Statement and Balance Sheet:

1. Hierarchical Structure: Consider arranging Account Groups hierarchically, starting with broader categories and narrowing down to specific account types. While it’s essential to have specific Account Groups, avoid creating too many. Over-segmentation can lead to confusion and inefficiencies. Optimal structure - 2 or 3 Levels.

Examples 5-6

2. Logical and simple numbering: Many companies attempt to align the numbering of account groups with that of individual accounts, but this isn't necessary. In fact, it can sometimes complicate the understanding of the underlying logic of account groups. Keep numbering concise to facilitate clearer communication with all stakeholders.

3. Clear Naming: Each Account Group should have a clear and descriptive name to avoid ambiguity. This helps in faster identification and reduces errors.

4. Include Descriptions: For each Account Group, include a brief description or guideline to clarify its purpose or the type of accounts it should contain.

Example 7

5. All industries: Ensure representation of all industries in which the Group's companies operate.

6. Similar revenue or expense: Account groups contain accounts with similar revenue or expense. Often, companies are tempted to name Account Groups based on reporting subtotals, such as “Indirect expense” or “Administration expense.” However, it's best to focus on logically grouping similar revenue and expense. With a well-structured COA and Dimension setup, generating a range of reports with preferred subtotal names will be straightforward.

Example 8

7. Cross-Referencing: If implementing in a reporting system, ensure that you can cross-reference Account Groups easily. Clearly structured Account Groups simplify tasks like setting user access rights, establishing budgeting permissions, or crafting reporting templates. Instead of dealing with individual accounts, you can efficiently manage them using Account Groups.

Example 9

8. Flexibility: Structure the Account Groups in a way that allows for future expansion of the business if new industries and new accounts have to be added to the Group CoA.

9. Regular Review: As businesses evolve, your financial data might too. Regularly review and update Account Groups to ensure they remain relevant and comprehensive.

10. Involve Stakeholders: Involve key stakeholders in the decision-making process when defining or revising Account Groups. This can include representatives from finance, operations, sales, and more.

Setting Up Accounts

When Account Group structure has been marked, continue with defining the Accounts. The guidelines to consider defining Accounts in the Group COA:

1. Logical, simple and hierarchical numbering: Using a simple numbering system can be beneficial. For instance, all non-current assets accounts in BS might start with '1', current assets accounts with '2', shareholders' equity accounts with '3', non-current liabilities with '4', current liabilities with '5', income accounts in P&L with '6', and expense accounts in P&L with '7'. Leave '9' for various adjustment accounts (IFRS, GAAP, Group adjustments) and cost allocation accounts. This aids in a logical grouping of accounts. Keep account numbering short to facilitate clearer communication with all stakeholders - usually 5 characters in account code are sufficient. All account numbers should be of the same length for easier data processing by the reporting system.

2. Clear Naming: Avoid overly complex account names. They should be straightforward, concise, and easily recognizable.

3. Flexible & Scalable Structure: As the business evolves, the Group COA should be able to adapt. Create a structure that allows for the addition of new accounts without a complete overhaul. For clarity and organization, allocate a distinct range of account numbers to each account group.

Example 10

4. Consistency: Ensure naming conventions, numbering sequences, and account types are consistent across the Group COA. This makes it easier to expand, integrate, or restructure the Group COA in the future. In Example 10, the account numbering for different WHT expense maintains consistency across the account groups.

5. Regular Review: Regularly review and refine the Group COA to ensure it aligns with the current and future needs of the business.

6. All industries: Ensure representation of all industries in which the Group's companies operate. For instance, if the group includes companies from diverse sectors like Lending and Construction, the Group COA has to include income and expense accounts for both industries.

Example 11

7. Statutory and regulatory requirements: The Group COA should clearly identify the accounts where revenue or expense recognition adheres to local statutory norms for the group's legal entities. Such accounts can be designated with Account type 'Local'. Data for 'Local' accounts are imported from the accounting or ERP systems of individual Group entities and reflect the true financial state of each separate legal entity. The selection of Account type 'Local' in the reporting system would generate the reports in accordance with statutory requirements.

Examples 12-13

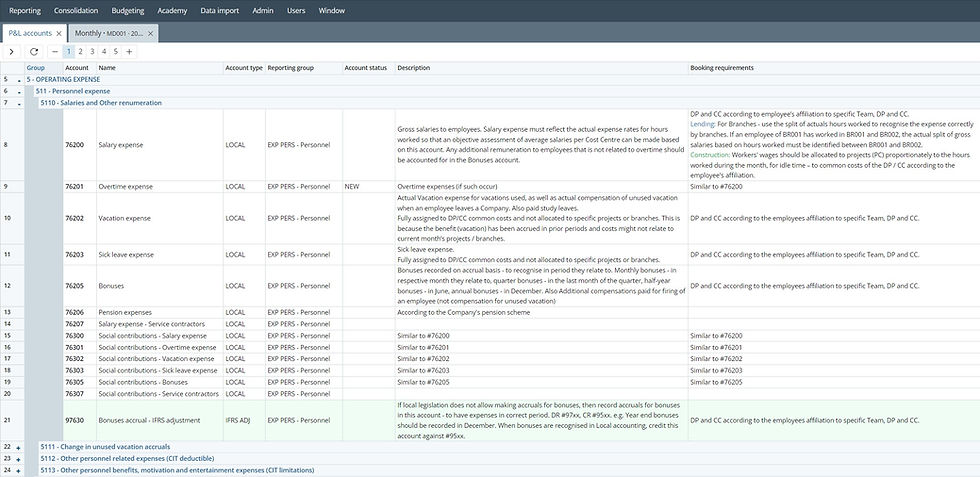

8. Management reporting requirements: When preparing Group COA it is very important to understand management needs and requirements for reporting and for KPI calculations. Ensure that the required information will be addressed either by the Group COA or the Dimension structure. In example below - management definitions how to organize Salary expense recognition in the Group COA.

Example 14

9. Operational Insight: Engaging operational-level managers is crucial, as they have to understand the revenue and expense accounts they are responsible for. Accounts must be clearly defined and intuitive, allowing these managers to quickly discern the components of a particular account. Such clarity not only fosters accurate budgeting but also enhances variance analysis. In the example provided, all vehicle-related expense accounts were refined in collaboration with fleet managers across the group.

Example 15

10. Tax Related Considerations: Engage Group tax managers to address any tax-related queries for the entire Group and to ensure that all essential tax-related information is available in the Group COA and in automated reporting.

Example 16

11. Alignment with Budgeting: For effective variance analysis, it's essential to match actuals in automated financial reporting with the budgeted numbers. When incorporating accounts into the Group COA, think about the budgeting process - is this account worth budgeting, who will oversee it and how permissions for budgeting will be set up in the reporting system.

Examples 17-19

12. Intra-Group Transactions: It's beneficial to establish separate accounts for intra-group transactions and balances. Primarily, it provides relevant and easy-to-read information to management and other report users about the value of transactions and balances with both external and Group companies. Additionally, this allows the reporting system to perform the necessary checks and eliminations of intra-group transactions and balances, as well as to create automated consolidated reports. In the Example 20 below, these accounts are categorized under the account type "Local / Intra-Group." Such accounts accommodate transactions with group companies as per local statutory guidelines. Data for 'Local / Intra-Group' accounts also are imported from the accounting or ERP systems of individual Group entities.

Example 20

Businesses often have concerns about the legal status of group companies. For instance, while some legal entities might not be legally integrated into the group, they might still be recognized as part of the group for managerial reporting and consolidation. In such cases, if the reporting system is advanced enough, I would suggest to record the transactions with these entities in intra-group accounts and create in the reporting system two types of consolidation reports: 1) Consolidation for Management Reporting: Includes all legal entities, treating them as part of the group. After eliminating intra-group transactions, balances in the intra-group accounts should net to zero. 2) Consolidation for Statutory Reporting: Excludes entities not legally part of the group. Post elimination, balances with these entities will still appear in intra-group accounts and be part of the group's revenue, expense and external balances.

13. Efficient Cost Allocation: The Group COA needs to include specific accounts designed for cost allocation to aid in activity-based costing (ABC) and profitability analysis.

In the Example 21 below these accounts are grouped under the "Local / Allocation" account type. While allocation accounts in the P&L statement always balance to zero and don't impact statutory reporting, they provide valuable insights into the actual costs of cost centres and the true profitability of projects, products, or other profit centers, without altering the overall net result of a separate legal entity.

It's highly beneficial when the reporting system can automatically carry out cost allocation based on predefined rules and formulas. To differentiate between allocation bookings made directly in the reporting system and the "Local" accounts that get data from separate legal entity accounting systems, it might be prudent to use different account numbers for "Local / Allocation" accounts. For instance, in the example 21 provided, account numbers starting with 99xxx are utilized.

Examples 21-23

14. Compliance with IFRS or GAAP Requirements: To guarantee seamless automated reporting in line with IFRS or GAAP requirements, the Group COA must incorporate accounts designated for related adjustments. In the examples provided above you will notice that all IFRS adjustment accounts are categorized under an account type labeled 'IFRS adj'. When generating reports in accordance with IFRS, the 'IFRS adj' accounts are added to the 'Local' accounts. The automated reporting process becomes more efficient if these adjustments can be booked directly into the reporting system for all relevant legal entities. Moreover, the ability to automate these bookings in the reporting system through predefined rules and formulas offers a substantial advantage. For logical distinction in numbering, while the first digit could be '9', the subsequent digit might indicate the Balance sheet or P&L statement item being adjusted. For instance, '91xxx' - IFRS adjustments for non-current assets, '92xxx' - for current assets, '93xxx' - for equity, '94xxx' - for non-current liabilities, '95xxx' - for current liabilities, '96xxx' - for income, and '97xxx' - for expense.

Examples 24-25

15. Compliance with Group Requirements: When Group reporting deviates from Statutory or IFRS (or GAAP) standards, it's essential to integrate accounts specifically designed for Group adjustments within the Group COA. Such accounts can be categorized under the 'Group Adj' account type. Although certain reporting systems offer the option to implement diverse group adjustments (like accruals) directly within the 'Local' accounts, it's not the most recommended approach. Doing so can distort the Statutory figures, resulting in discrepancies between the reporting system's statutory results and the actual statutory reports from individual legal entities.

Examples 26-27

16. Foreign Currency Translation Reserve: If you aim to analyze a separate legal entity's data in both their 'Local' functional currency and the reporting currency, it's essential to include an account for the foreign currency translation reserve.

Examples 28-29

17. Streamlined Consolidation: Similar to the above, accounts vital for consolidation ( e.g. goodwill, impairment of goodwill, non-controlling interest) are integrated into the Group COA. It's important that the reporting system can handle consolidation entries and, ideally, that such entries can be automatically executed using predefined rules and formulas. Highly sophisticated reporting systems offer the capability to make consolidation eliminations and adjustments not only at the account level but also across all requisite dimensions. This advanced feature enables the generation of consolidated management reports, even those segmented by products.

Examples 30-32

Tips for Implementing the Group COA

Implementing the Group COA within Group companies typically follows one of two main scenarios:

Full Adoption: Separate legal entities take on the Group COA as their primary Local COA, replacing their previous Local COA.

Mapping & Adjustment: The entities fine-tune their existing Local COAs to align with the Group's standards and create a mapping between the Local and Group Chart of Accounts.

Both strategies come with their distinct set of advantages and potential challenges - a topic that is explored in another detailed article.

Discover how to implement Group requirements in the article: 'Successful Implementation of a New Group Chart of Accounts (Group COA) Across the Group'.

However, irrespective of the chosen path, a few pivotal considerations can smooth out the implementation of the Group COA:

1. Accessibility & Involvement: First and foremost, the new Group COA needs to be readily accessible to all legal entities and involved stakeholders. Ideally, this involvement should extend to the creation or review phase of the Group COA. Such early engagement ensures that the COA resonates well with its users, is easy to use, and no critical aspects are overlooked. A practical approach might be to house the Group COA within the reporting system. Such an arrangement would ensure that stakeholders can effortlessly access it, always in line with their designated access rights.

Examples 33-34

2. Training & Understanding: With a new Group COA in place, comprehensive training becomes indispensable. It ensures that all entities grasp the nuances of the new requirements.

3. Search Functionality and Comprehensive Descriptions: Detailed descriptions of accounts enhance the accuracy of bookings, facilitating a deeper comprehension of actual data and more precise budgeting. Moreover, having a robust search function ensures quick answers, streamlining decisions about where specific expenses should be recorded or allocated in the budget.

Example 35

4. Visible Mapping of Local Accounts to Group Accounts: For Group entities utilizing the mapping approach, executing this mapping directly within the reporting system would offer distinct advantages:

Data Validation: Certain reporting systems ensure accurate data validation, confirming that all data imported from Local accounting and ERP systems aligns correctly with the Group COA.

Real-time Mapping Adjustments: Advanced reporting systems can adjust "on the fly." This means that if any mapping alterations occur, all data and reports within the system are instantly updated, eliminating the need for data re-imports.

Dual View Capability: Reporting systems may permit viewing of both Local and Group accounts. This feature enhances clarity for Local entities, helping them understand their data in greater depth.

Examples 36-38

Every topic touched upon in this article holds layers of complexity and depth when it comes to crafting a Group COA tailored for a specific company. A single article can't capture all the nuances -given that every company is a distinct and demand a uniquely crafted COA. Take the time to define the perfect Group COA; armed with the knowledge from this article, you now know HOW! By doing so, you will make a foundational step towards achieving streamlined and effective financial reporting automation meeting the diverse reporting requirements: be it Statutory, IFRS, GAAP, Group, Management reporting, or Consolidation.

Comments